Motorists in Britain should brace for another year of steep insurance rises as providers confront cost pressures, industry figures have warned.

Admiral Group Plc will continue increasing motor insurance prices and expects the rest of the market to follow suit, Chief Executive Officer Cristina Nestares said in an August earnings call. The view of one of the UK’s largest general insurers is reflected in a report by EY predicting a 16% rise in prices in 2023, followed by a 11% jump in 2024.

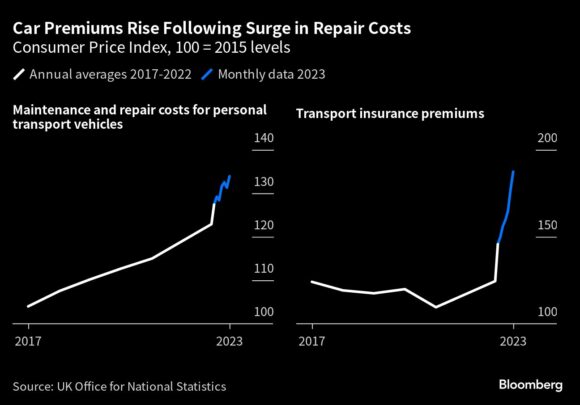

Car insurance is one of the starkest examples of cost inflation in the UK, where across the economy price rises are starting to ease from the four-decade highs of last year. Transport insurance prices rose almost 50% in the year to July, according to data from the Office for National Statistics. The Association of British Insurers said average car cover reached £511 in the second quarter — the highest price tag since it started collecting the data in 2012.

Yet insurers are still struggling, with EY predicting that insurers will spend £108.50 for every £100 taken in premiums in 2023, signifying a slight improvement but an overall loss. The firm expects profitability to return in 2024.

Aviva Plc was a notable bright spot this earnings season, reporting first-half results that were slightly ahead of analyst expectations, partly through a focus on “pricing appropriately.” Still, the pace will likely be tough to sustain due to claims inflation, which is making general-insurance underwriting harder than usual, as well as market pressures on its life insurance unit, according to Bloomberg Intelligence analysts. Aviva’s share price is down 15% since the start of the year.

Direct Line Insurance Group Plc shares, meanwhile, have fallen around 28% so far this year after several profit warnings and the resignation of its CEO in January. It’s due to report its latest outlook on costs at its half-year results on Sept. 7.

“Although CPI is forecast to reduce at the end of this year, if you look at the factors explaining why claims are going up, those factors aren’t going to change over the coming 12 months,” said Mohammad Khan, who leads PricewaterhouseCoopers’s general insurance practice in the UK.

Perfect Storm

The soaring cost of fixing a vehicle and longer repair times are partly responsible for insurers’ rising expenses, according to an Admiral spokesperson.

The war in Ukraine closed production facilities and pushed up the price of spare car parts. The cost of replacement parts for some popular car models increased by as much as 21%, while car repair prices rose 33% over the last year, according to ABI data.

A shortage of mechanics in the UK has also led to labor costs rising as much as 40% for some insurers over the past year, the ABI said.

It’s also more expensive to pay for treatment for injuries sustained in accidents as both the cost of manufacturing drugs and transporting them into the UK has gone up, according to Khan. “We’re basically in a perfect storm,” he said.

Consumers Under Pressure

It’s not just that claims cost more, but also that consumers are claiming more often. Drivers are spending more time on the road, as workers return to the office and Britons embark on more post-pandemic travel in general.

“When we look at premium increases it’s important to see them in context and highlight that they are starting from a very low base,” an Admiral spokesperson said in an email. “During COVID, premiums fell as lockdown restrictions meant that fewer people were driving and claims frequency fell.”

Some consumers are responding to higher premiums by switching to cheaper plans or purchasing less generous cover. The latter is risky as it means they’re going to get less back from the insurer if they make a claim.

Admiral saw a 7% year-on-year reduction in UK motor customers in the first half, as customers respond to rate increases over the last 15 months, according to a recent earnings presentation. Still, higher rates helped the company increase revenue and push up average premiums.

Insurers are also responding by adding cheaper options to their offering, for example allowing consumers to remove windscreen cover. Underwriters are also investing in technology and repair networks to gain more control and stability over prices.

“We recognise that these are challenging times for many people,” Admiral said.

Photograph: Heavy traffic makes it way along Park Lane during a national rail strikes in London, UK, on Wednesday, Oct. 5, 2022. Photo credit: Chris J. Ratcliffe/Bloomberg

Topics Carriers Trends Auto Pricing Trends

Was this article valuable?

Here are more articles you may enjoy.

Unusually Warm Atlantic Ocean Is Supercharging Hurricane Idalia

Unusually Warm Atlantic Ocean Is Supercharging Hurricane Idalia  3M Agrees to Pay More Than $5.5 Billion Over Military Earplugs

3M Agrees to Pay More Than $5.5 Billion Over Military Earplugs  Billion-Dollar Satellite Risks Upending Space Insurance

Billion-Dollar Satellite Risks Upending Space Insurance  Chubb Loses Bid to Enforce D&O Coverage Exclusions in Opioid-Related Case

Chubb Loses Bid to Enforce D&O Coverage Exclusions in Opioid-Related Case